Irrational marketing

It’s wise to reflect that marketers are susceptible to the same mental shortcuts

The discipline of behavioural economics has given marketers another lens through which to peer at, and seek to understand, consumers. Never mind what people say in focus groups or do in ethnographic videos, the irrationality of their decisions can be understood as a series of heuristics – cognitive rules of thumb – that must have made sense in mankind’s savannah past, even if they seem at odds with the modern world.

The principle of “hyperbolic discounting”, for example – an extreme preference for modest payoffs now relative to greater ones in the future – would have been perfectly logical when lives were “nasty, brutish and short”. If it clings on today, when deferred gratification would generally be the smarter strategy, it’s because evolution hasn’t had a chance to catch up.

But before we smile too long at consumer irrationality and pat ourselves on the back as we manipulate their choices with our cleverly conceived “nudges”, it’s wise to reflect that marketers are descendants of that same savannah and are susceptible to the same mental shortcuts.

That big decision you and your team made recently – the new positioning, the architecture revamp, the department restructuring: was it really the product of sober, evidence-based reasoning, as you tell both yourself and the board, or could it perhaps have been swayed by one of these five behavioural economics principles?

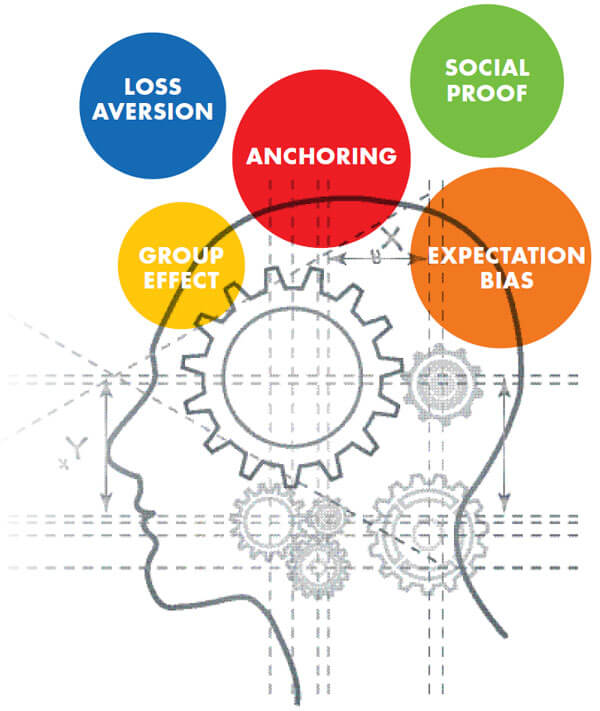

1. LOSS AVERSION

We have the fathers of the discipline – Daniel Kahneman and Amos Tversky – to thank for this one. They showed that people tend to place a greater value on what they already possess over the acquisition of the same “good”.

In marketing circles, you see the principle in action when teams struggle to cull an overburdened product range. You can hold up an SKU and get agreement that they wouldn’t invent it if it didn’t exist but, somehow, reasons will always be found to save it.

2. ANCHORING

An example of a “priming” effect, where the first piece of information received – generally a number – exerts undue influence on eventual decision-making.

Marketers get primed when looking at metrics such as net promoter score. They will invariably start with the category average and consider strategies to improve the brand’s number from there. If the category happens to be something unpopular, such as banking, all the NPS scores will be negative – so a slightly better negative seems OK.

Trouble is, consumers don’t live in one category. So it would be better to decide on an absolute, rather than relative, target – and make it ambitious.

3. GROUP EFFECT

In his book Going to Extremes, Cass Sunstein showed that a group will tend to exaggerate any slight bias that was there at the outset. So pernicious is this that, by the end of the session, the overall group bias will be more extreme than that of the single most-biased member beforehand.

For its application in marketing, look no further than the workshop. Teams will gather to discuss positioning options and there will be a mild tilt towards one at the beginning. Come close of play, even the doubters will be rabid zealots.

4. SOCIAL PROOF

That big-budget, “emotional epic” commercial you just signed off: it was based on what came out best from research, right? Nothing to do with the fact that every other marketer out there is investing in the same kind of spot.

The tendency to do what others do, rather than stand out of line with what’s best, is something we all need to watch.

5. EXPECTATION BIAS

Or: the tendency to believe data that agrees with your expectations and to disbelieve, disregard or downgrade data that doesn’t.

Think about all those marketers bent on prioritising a digital communications strategy – despite the average of six clicks per 10,000 ads; despite the click fraud, the botnets and the evidence that less than half of all internet ads are seen by humans; despite the admission of Procter & Gamble, the world’s biggest advertiser, that a “precision”, digital approach cost it customers.

Behavioural economics is fascinating when we apply it to others – like seeing them unfairly, naked and defenceless. Just occasionally, though, and no matter how unflattering it seems, it can be wise to hold up a mirror to ourselves.

Daniel Kahneman and Amos Tversky

Now the subject of a book by The Big Short author Michael Lewis, the pair teamed up at The Hebrew University of Jerusalem, publishing their first joint paper, Belief in the Law of Small Numbers, in 1971. They went on to develop the cognitive bias ideas of anchoring and prospect theory, for which Kahneman was awarded a Nobel Prize in 2002 – Tversky having died six years earlier. In 2011, Kahneman packaged some of their most seminal theory in runaway bestseller Thinking, Fast and Slow.

Richard Thaler and Cass Sunstein

They authored Nudge: Improving Decisions About Health, Wealth, and Happiness, the book that influenced David Cameron to set up a behavioural insights team at No10.

Dan Ariely

The professor of psychology and behavioural economics at Duke University, North Carolina, has the gift of popularising arcane academic theory. Two of his books have made The New York Times’ bestsellers list: Predictably Irrational and The Upside of Irrationality.